GBP Down After Carney’s Remarks, Riksbank Decides on Policy

The dollar traded lower yesterday, and although EU and US indices rose, the Asian ones closed in negative territory today. It seems that investors may have turned cautious again as the outcome from the Trump-Xi meeting is far from suggesting that the world’s two largest economies have bridged their differences. The pound was the main loser among the G10s perhaps due to the disappointment in the UK construction PMI for June, as well as comments by BoE Governor Mark Carney. As for today, the Riksbank is scheduled to decide on monetary policy.

Risk Appetite Softens, Pound Slides as Carney Sounds Cautious

The dollar traded lower against most of the other G10 currencies on Tuesday and during the Asian morning Wednesday. It gained only against GBP, while it was found virtually unchanged versus EUR and NZD. The main winner was JPY, with AUD taking the second place, but well behind.

The weakening of the dollar and the strengthening of the safe-haven yen suggest that optimism surrounding the outcome of the Trump-Xi meeting has faded somewhat. Although major EU and US stock indices ended their sessions in the green, the gains were modest compared to Monday. The exceptions were Italy’s FTSE MIB, which accelerated perhaps to catch up after rising only 0.09% on Monday, and UK’s FTSE 100, which may have gained due to the weak pound. Remember that many companies of the index generate profits in other currencies, so in a weakening GBP environment, if those profits are converted to pounds, they worth more. The softening risk sentiment was more evident in Asia today, where most indices finished in the red. Japan’s Nikkei 225 and China’s Shanghai Composite closed 0.53% and 0.94% down respectively.

As we noted yesterday, investors may have ended the party early as the outcome from the Trump-Xi meeting is far from suggesting that the world’s two largest economies have bridged their differences. It just takes us back at the beginning of May, just before the latest round of tensions. Most of the difficult issues are still outstanding, and although fresh tariffs have been postponed, the previously imposed ones are still there, which could keep weighing on global growth. What’s more, overnight reports that the staff of the US Commerce Department was told that China’s tech giant Huawei should still be treated as blacklisted suggest that there is still a long way to go before the two nations agree on a final deal.

Back to the currencies, the pound was yesterday’s main loser, perhaps due to the disappointment in the UK construction PMI for June, as well as comments by BoE Governor Mark Carney. Kicking off with the construction PMI, the index tumbled from 48.6 to 43.1, its lowest since April 2009, missing estimates of a rise to 49.3. This followed a similar disappointment in the manufacturing index on Monday, which slid to 48.0 from 49.4. Today, we get the more-important services index, where another slide may raise more concerns with regards to the performance of the UK economy during the second quarter. Remember that following the April monthly GDP figure, which showed that the economy contracted 0.4%, the NIESR projected a 0.2% contraction for Q2, while the BoE revised its estimate for the quarter lower, to stagnation from a +0.2% qoq growth.

Now, speaking about the BoE, let’s pass the ball to its Governor, Mark Carney. Despite reiterating the view that higher rates may be needed in the event of a smooth Brexit, BoE’s Chief noted that a global trade spat and a no-deal Brexit are growing risks for the UK economy. It seems that, even though the BoE remains among the few major central banks willing to increase rates, the approach has become more cautious. With the chances of a no-deal Brexit staying decent, and data suggesting that the uncertainty surrounding the UK’s departure out of the EU is weighing on the British economy, investors have added to bets over a cut by the end of the year after Carney’s speech. According to the UK OIS (Overnight Index Swaps), the probability for such an action has risen to 51.1% from 40%.

Moving ahead, we still believe that the path of least resistance for the pound is to the downside. With the UK’s next Prime Minister yet to be decided, and both of the remaining candidates signaling that they could go for a no-deal divorce at the end of October if no other solution is found on time, investors are finding it hard to believe that a BoE hike could materialize. Even if the UK departs in an orderly manner on October 31 st, up until then, the uncertainty surrounding the process may weigh further on the domestic economy and thereby, force BoE policymakers to abandon plans for higher rates well ahead of the exit.

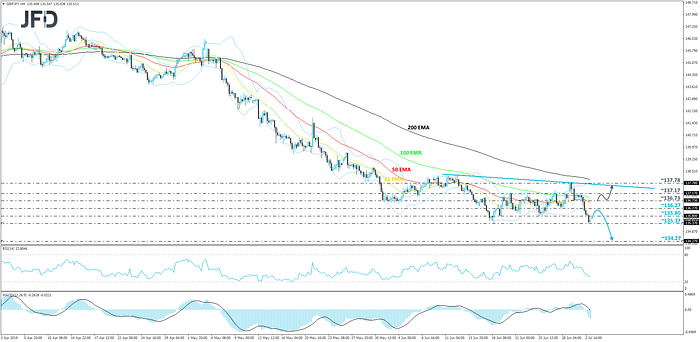

GBP/JPY — Technical Outlook

From the start of this week, GBP/JPY keeps on drifting lower, trading now below a short-term tentative downside resistance line taken from the high of June 11 th. We can see that today, the pair stopped its freefall near the 135.37 hurdle, which held the rate from moving lower on June 18 th. Given that the pair is quite extended to the downside already, especially on the shorter timeframes, we may see a small correction back up and then another leg of selling, which is why we will stay cautiously-bearish for now.

A rebound from the above-mentioned 135.37 support area could push the rate back up to the 135.80 zone, which was previously seen as a good support on June 19 thand 25 th. GBP/JPY could climb a bit higher and test the 136.27 hurdle, marked by the low of June 28 th. That hurdle could take on the role of becoming a good resistance level, and if it holds, the bears could jump in and drive the pair to the downside again. If the rate slides below the 135.37 obstacle, the pair would confirm a lower low and may travel all the way down to test the 134.27 level, marked by the intraday swing low of January 3 rd.

On the other hand, if the rate moves back above the 136.73 barrier, marked by the inside swing low of July 1 st, this would also place the pair above most of its EMAs on the 4-hour chart. This is where more bulls might help GBP/JPY to travel a bit higher, to test the 137.17 hurdle, which marks the yesterday’s high. If the rate acceleration doesn’t stop there, the pair may continue going for a larger correction, bringing it closer to the aforementioned downside line, which might help to keep GBP/JPY down, at least for a while.

Will the Riksbank Push Back its Forward Guidance?

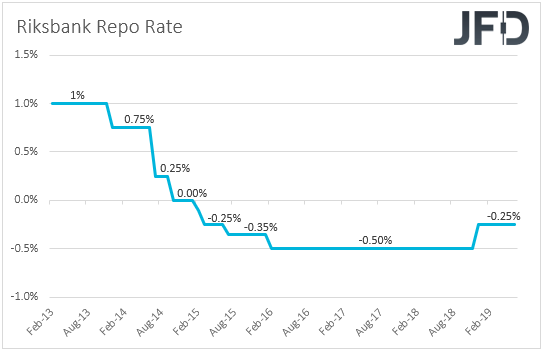

Following the RBA decision yesterday, today the central bank torch will be passed to the Riksbank. At its latest meeting back in April, the world’s oldest central bank kept its repo rate unchanged at -0.25% and decided to push back the timing of when it expects interest rates to rise further, noting that this could happen “towards the end of the year or at the beginning of next year”. Since that meeting, Swedish data were mainly on the bright side, with GDP slowing by less than anticipated in Q1 and inflation accelerating. It is worth mentioning that the core CPIF rate, which excludes the volatile items of energy, ticked up to +1.6% yoy in April from +1.5% in March, and then rose to +1.7% in May.

Seen in isolation, the data suggests that the Bank could keep its forward guidance unchanged at this meeting. However, bearing in mind that the Riksbank has been usually following the footsteps of the ECB, we believe that there is a decent chance for a push back, perhaps for officials to take off the table the “end of the year” part. Remember that at its latest gathering, the ECB decided to push back its own forward guidance, while two weeks ago, President Draghi said that additional stimulus will be required if a sustained return of inflation to the ECB’s aim is threatened. That said, although we see the case for the Riksbank to close the door to a 2019 hike, given the decent Swedish data, we don’t expect policymakers to start signaling a cut, at least not yet.

As for the Swedish krona, it could slide if officials decide to push back the timing of when they expect interest rates to rise, but in the absence of any cut signals, those loses are likely to stay short lived. At a time when other major central banks are cutting rates, or signaled that they could do so, a Riksbank still willing to hike, even at a later stage, could prove supportive for the Swedish currency. In order for SEK to plummet and stay under selling interest, officials would have to totally abandon any hike plans, and maybe turn their eyes to the cut button.

USD/SEK — Technical Outlook

After reversing to the downside in the end of May, USD/SEK has been trending lower, with occasional corrections to the upside. The pair still remains below a short-term downwards moving resistance line taken from the high of May 23 rd. That said, after another strong slide at the end of June, the rate found good support near the 9.2469 zone, from which it rebounded last week. From Monday, USD/SEK started recovering some of its losses made during the second half of June, but got held near a strong resistance barrier, at 9.3715, which is the low of June 7 th. We believe that the pair could continue feeling the bear-pressure and could move lower once again, hence why we will stay somewhat bearish, at least for now.

A drop below the 9.3233 obstacle could open the door to slightly lower areas again, like the 9.2776 hurdle, marked by Monday’s low. Even if the pair rebounds back up a bit from that hurdle, as long as it stays below the 9.3233 area, we will continue targeting the downside. If this time the bears manage to push the pair further down, below the 9.2776 mark, such a move could lead the rate to the above-mentioned 9.2469 zone, marked near the low of last week.

Alternatively, if USD/SEK climbs above 9.3715, which is the current high of this week, this might open the door for a slightly bigger correction to the upside. The pair may then travel to the 9.4346 zone, marked by the high of June 21 st, which would also place the rate above the 200 EMA on the 4-hour chart. Although we could see the pair retracing back down after hitting that zone, if the bears are not capable to regain full control, USD/SEK might push back up a bit more. A break above the 9.4346 area could allow the rate to move towards the 9.4580 level, marked by the low of June 18 th, or even slightly higher, to test the aforementioned downside resistance line.

As for the Rest of Today’s Events

During the European day, we get the final services and composite PMIs for June from the Euro-area nations of which we got the manufacturing prints on Monday. As we already noted, the UK services PMI for the month is also due to be released.

In the US, markets will close early as it is the Independence Day Eve. We do however get some US data. The ADP employment report for June is scheduled to be released, and expectations are for the private sector to have gained 140k jobs, more that May’s poor 27k. This could raise speculation that the NFP print, due out on Friday, may also rebound from its previous soft figure of 75k. That said, we repeat for the umpteenth time that, even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are considered) has been low in recent years. Taking into account data from January 2011, that correlation now stands at 0.47%. The final Markit services and composite PMIs for June, the ISM non-manufacturing index for the month, the trade balance for May, and initial jobless claims for the week ended on June 28 thare also due out.

As for the speakers, we have two on today’s agenda: BoE Deputy Governor for Monetary Policy Ben Broadbent and BoE Deputy Governor for Financial Stability Jon Cunliffe. Following Governor Carney’s remarks, it would be interesting to hear whether these members will also appear concerned with regards to global trade and Brexit.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

70% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure .

Copyright 2019 JFD Group Ltd

Originally published at https://www.jfdbank.com on July 3, 2019.